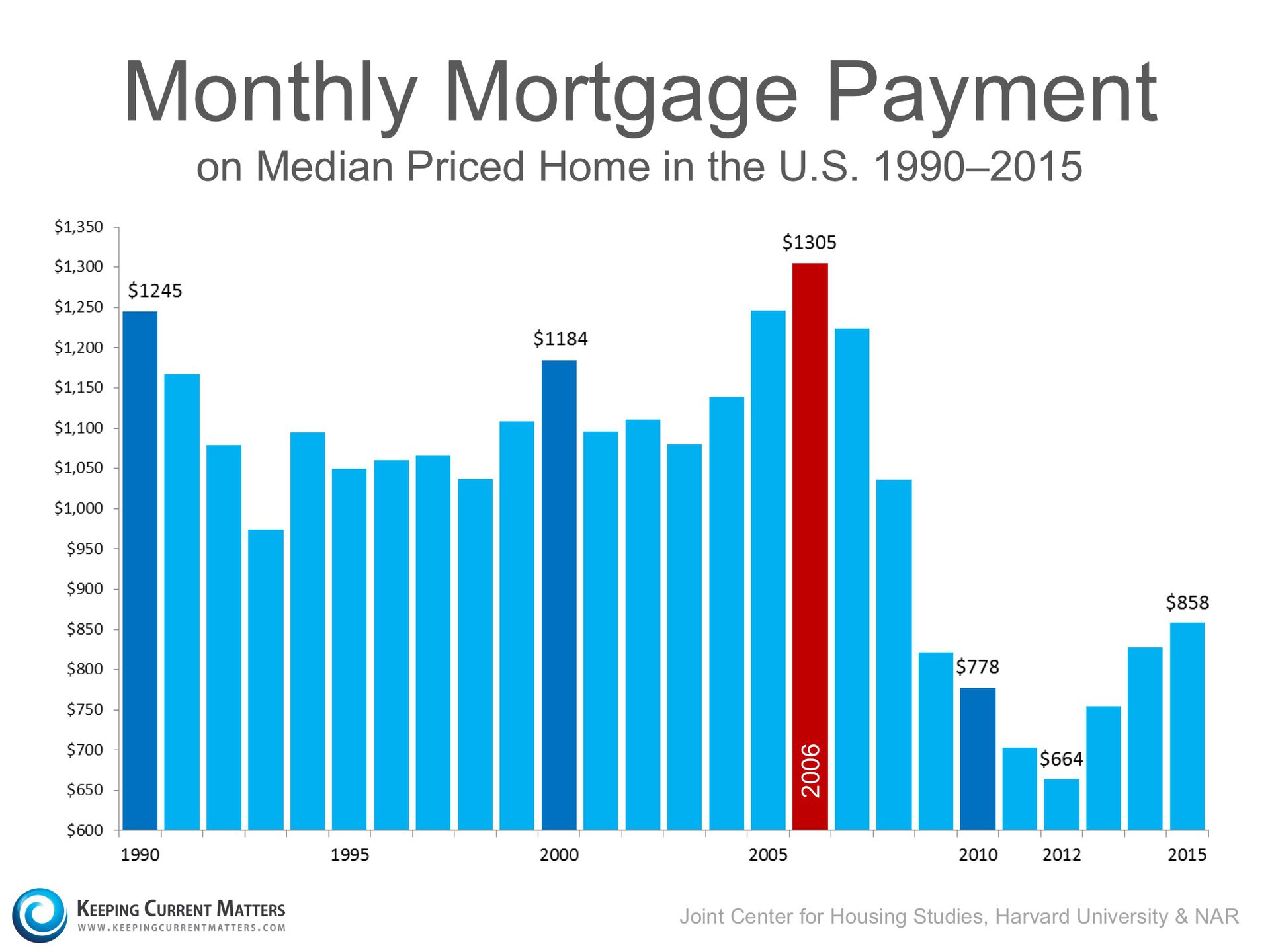

“Even though home prices are climbing far above people’s income, exceptionally low mortgage rates have permitted people to buy a home without overstretching their budget. For someone making a 20% down payment, the monthly mortgage payment at today’s mortgage rates would take up 15% of a person’s gross income. During the bubble years, it was reaching 25% of income. The long-term historical average is around 20%. Therefore, a middle-income household does not need to overstretch their budget much if at all to buy a typical home.”

This paradise is a dream destination for those seeking luxury, exclusivity, and a captivating lifestyle.

This county in Florida is renowned for its luxurious golf course communities.

In a market where presentation, strategy, and relationships define outcomes, choosing the right team isn’t optional, it’s everything. At the Malloy Home Team at SERHANT., we don’t just list homes. We position them. We don’t just find properties. We secure opportunities others never see.

114 N Coastal Way Jupiter, FL 33477